We’d need 4.6 million new apartments by 2030 to meet demand for rental living and keep prices in check, reports the National Multifamily Housing Council. That’s about 373K new units each year on average, a number that’s rather optimistic considering the pace of apartment construction in the last decade. So how feasible is this plan? A recent study from RentCafe on the apartment market suggests the country’s growing renter population need not be too concerned.

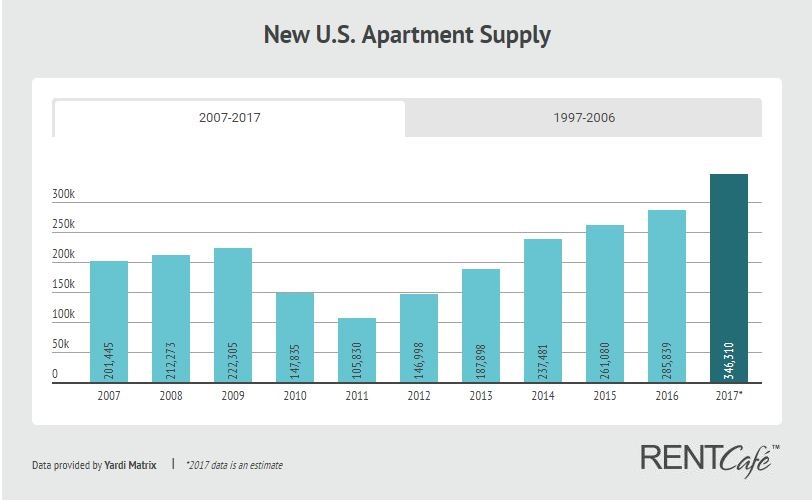

According to data from real estate data provider Yardi Matrix, apartment construction is at a 20-year high, with most of our country’s biggest cities seeing significant upgrades in rental stock. After a slow post-recession period, the market started rebounding in 2012 and by 2014 new supply had amounted to more than 237,000 units delivered in one year, well above historical averages. Between 1997 and 2006, annual completions averaged 212,740 units.

In 2017, apartment completions are expected to top 345,000, a 21% increase compared to last year’s deliveries when more than 285,000 units saw the light of day.

Hot Urban Markets See Rents Softening as Developers Ramp Up Apartment Construction

After peaking in 2014 at 5.1%, monthly rent prices rose just 1.5% to $1,316 in May, the lowest annual growth rate we’ve seen in more than three years. In 2017, the average U.S. rent is expected to increase a modest 3.9%.

Does this mean apartment prices are finally taking a break from rent growth? Apparently so, and thanks to intensified apartment construction, that’s even the case with some of the country’s historically tight (or rather outrageously expensive) markets. Close to 6,200 new units entered the San Francisco metro area in 2016, with approx. 5,400 apartments expected to be delivered this year and another 9,500 under construction. While demand is still strong in the city, this flood of new rentals coming online is finally putting a damper on the incessant rent growth that pushed rental costs up a whopping 49% in the last 5 years.

Rents in San Francisco have been slowing down for the last 10 months, with the pace of growth currently at its lowest level in the last 2 years. Rents in May 2017 were $2,497 in the SF metro, a meager 0.5% increase y-o-y. By comparison, in May 2016 annual increases stood at 6.2% and a year before rent growth was in double digits, approx. 11.9%.

And San Francisco isn’t alone in the rent deceleration game. Rents are cooling in other urban hotspots favored by young professionals such as Houston, Austin, Denver, and Portland. Additionally, 6 of the country’s top 10 priciest markets even experienced rent drops in May, including Manhattan, Boston, and San Jose.

“From an affordability standpoint, things are starting to look better for renters,” says Doug Ressler, Yardi Matrix senior analyst. “Rent growth is slowing down, even in the country’s most expensive markets and it doesn’t stop at that. With more units on the table, renters may be able to get some discounts and concessions on new leases, including one month of free rent, waived move-in fees, and free gym memberships.”

Want to read more about what’s trending in apartment markets across the country? Find the rest of this article here.